Equity compensation is now a common part of pay at technology companies, startups, and many public firms. Restricted stock units, stock options, and employee stock purchase plans can build real wealth over a career. They give you a stake in the company you help run.

They also carry risks that a salary and a cash bonus do not. The value of your equity rises and falls with one company. You often cannot sell your shares when you want to. And the tax rules behind them are dense enough that one timing mistake can cost you thousands. Below are three hazards that affect almost everyone who holds equity compensation, followed by how a single coordinated plan can manage them together.

Hazard 1: Concentration risk

Why it matters most

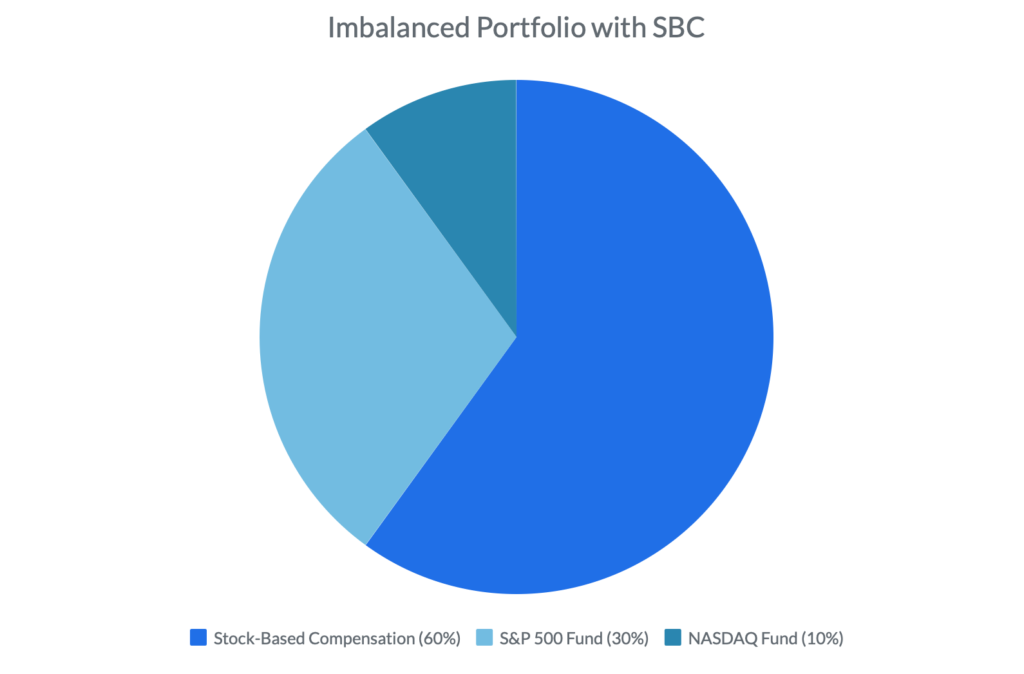

Concentration risk is the largest problem for most people who hold equity compensation, so it belongs first. The idea is simple. A large share of your net worth depends on the success of a single company, and that same company also pays your salary.

When your employer thrives, this feels wonderful. The trouble appears when the company struggles. A weak earnings report or an industry-wide slump can cut the value of your shares at the very moment your job feels less secure. You carry a double exposure that a careful investor would never take on by choice.

Many people deepen the problem without noticing. A software engineer who buys a broad market index fund picks up even more technology exposure on top of an already tech-heavy paycheck. The fund quietly doubles down on the sector that already dominates their financial life.

Hazard 2: Illiquidity

How it limits your choices

The second hazard is illiquidity, meaning your ability to turn shares into cash when you actually need it. Equity compensation often locks up value in ways that surprise people, and the constraints differ depending on whether your company is public or private.

If you work at a public company, your shares are tradable in theory. In practice, vesting schedules spread your grants across several years, and many employers set blackout periods that block trading around earnings dates. A company that has recently gone public may also hold employees to a lockup period of several months before anyone can sell. Your wealth exists on paper well before you can spend it.

If you work at a private company, the limit is sharper. No public market for your shares exists yet. You usually wait for an acquisition or an initial public offering before you can sell, and that event may be years away. Private secondary markets let some employees sell shares to outside investors ahead of an exit, though these transactions often need company approval.

Hazard 3: Tax complexity

Why it creates costly mistakes

The third hazard is tax complexity, and it catches even experienced people off guard. Each form of equity compensation follows its own rules for when income appears and how it gets taxed. Restricted stock units generally count as ordinary income when they vest. Stock options can carry alternative minimum tax consequences and strict timing rules. Some elections come with a short filing window after a grant, and you cannot reverse a missed deadline.

These decisions interact with one another and with the rest of your finances. The rules also shift over time, so a strategy that worked a few years ago may no longer be the best choice today. Many people learn these details only after an expensive mistake has already happened.

How financial planning helps with all three hazards

These three hazards rarely show up on their own. A decision to diversify raises a tax question. A tax move depends on whether you can sell. A liquidity strategy changes your concentration. Handle each one in isolation and your fix in one place tends to create a new problem in another. Managed inside a single plan, the same decisions reinforce one another, and the parts add up to more than they ever would apart.

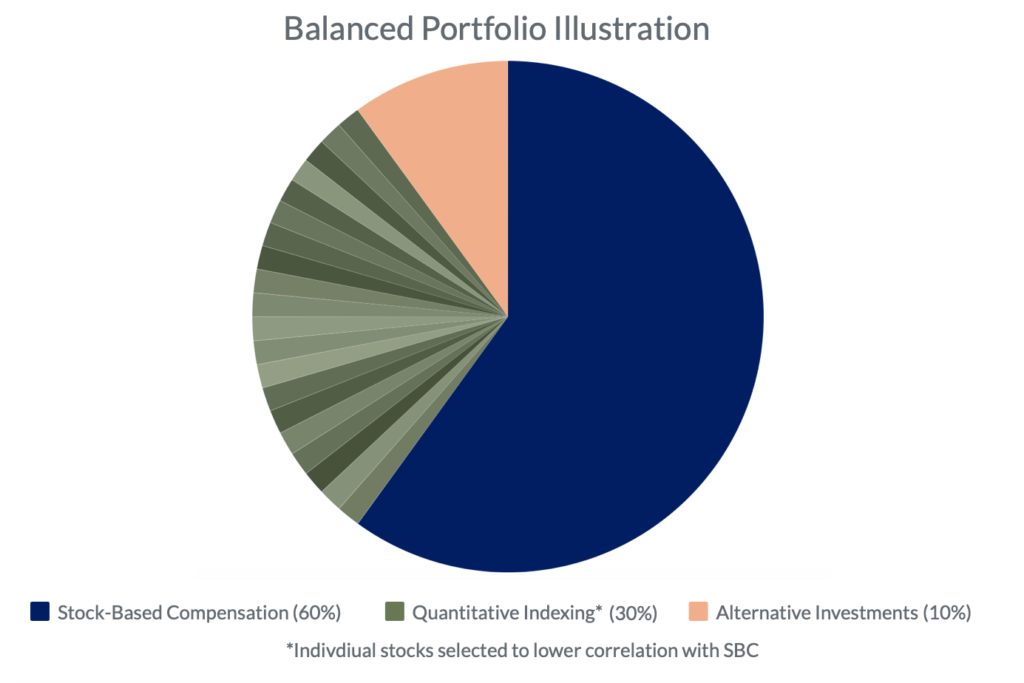

Quantitative Indexing for concentration risk

At Magnifina we address concentration with Quantitative Indexing. It centers on building and managing a portfolio of individual stocks that represent an index, held in your own account instead of through a fund. We can exclude your employer’s stock completely, reduce exposure to the sectors most correlated with it, and thus shape the rest of the portfolio toward companies with lower overlap with your equity compensation. You keep broad participation in the market while removing the excessive concentration risk from one large compensation package.

Customized structured solutions for liquidity and concentration

For a large position you cannot or would rather not sell outright, customized structured solutions can reduce the risk of that position and unlock cash from it at the same time, while postponing a sale. These arrangements are sophisticated, and they work best when they stay coordinated with your wider financial plan over time. Choosing and managing one well is exactly the kind of complex work we do with clients, and it is rarely something to handle on your own.

Tax planning coordinated with your CPA

We bring tax planning into your overall financial plan and coordinate with your CPA, whether that is your own accountant or one from our network, so your investments and your tax picture stay aligned. Timing matters a great deal with equity compensation, and looking ahead helps keep your options open.

How we bring the plan together

At Magnifina we specialize in individual stock investing grounded in business fundamentals and valuation, and we pair it with comprehensive financial planning. That combination lets us reduce the concentration risk that index funds can hide, fold liquidity strategies into the rest of your plan, and build tax-aware decisions in alongside your CPA. The same plan covers everything else that matters to you, such as retirement, funding an education, buying a home, and deciding how a future windfall fits your goals.

If you hold equity compensation and want to know whether our approach fits your situation, you can start with a quick survey. It is only four questions, and it helps us both see whether we are a good fit.