After taming inflation, the Fed aims for a soft landing

The market seems to have found a durable bottom in the fourth quarter of 2023. There was a strong rally at the beginning of November which included a wide variety of sectors and industries. Small and medium cap stocks benefited the most (as reflected by the indices), which contrasts significantly with their lagging performance over the previous year, as well as the narrow rally of last spring involving the tech giants. The businesses underlying small and medium stocks tend to be more sensitive to interest rates. We focus on these kinds of stocks and believe they provide great opportunities and value.

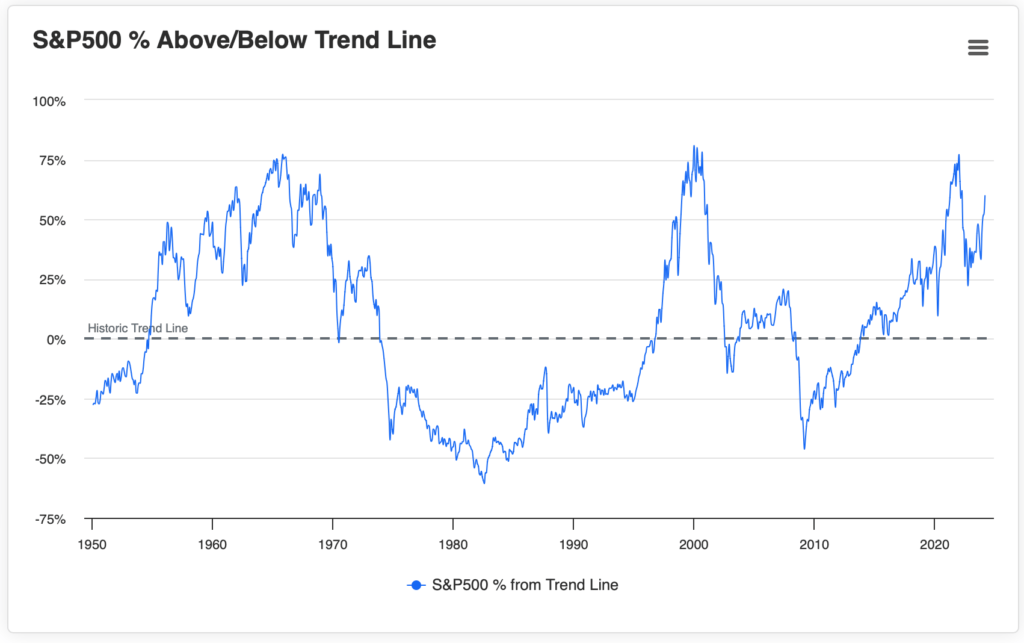

The long-expected recession still hasn’t arrived. The potential for weakness has caught the Federal Reserve’’s attention, however. In their December statement, the Fed indicated that they are anticipating 3 interest rate cuts toward the end of 2024. While the economy may remain healthy today, it’s worth remembering that rate cuts occur in response to an economic slowdown. A “soft landing” is the term given to a situation where the Fed manages to avoid a recession by acting right on time. These are rare, and the previous one occurred in 1995. (See chart below). The Fed is commonly perceived to react too late both to inflation and recession.

Looking ahead, we’re optimistic about the market. Just because the Fed sees the possibility for a slowdown, doesn’t mean it would occur soon. Additionally, there are some potential supports for the economy, which might help achieve a soft landing. These include pent-up housing demand and a wave of productivity gains from new technologies. There are of course risks to this scenario (including geopolitical risks), and we will continue to monitor new developments.

Active Manager Sentiment

April 4, 2024: 84.24% Aggregate Equity Exposure

After topping out at over 100% equity exposure, active managers trimmed positions to around 85% (in aggregate). We read this as a signal that the market was overbought in the short-term, but not necessarily a sign of longer-term weakness.

The NAAIM Exposure Index represents the average exposure to US Equity markets reported by members. NAAIM member firms are asked each Wednesday to provide a number which represents their overall equity exposure at the market close. Responses are tallied and averaged to provide the average long (or short) position of all NAAIM managers, as a group.

Disclosure: Magnifina is a frequent contributor to this index.

Stock Performance by Category

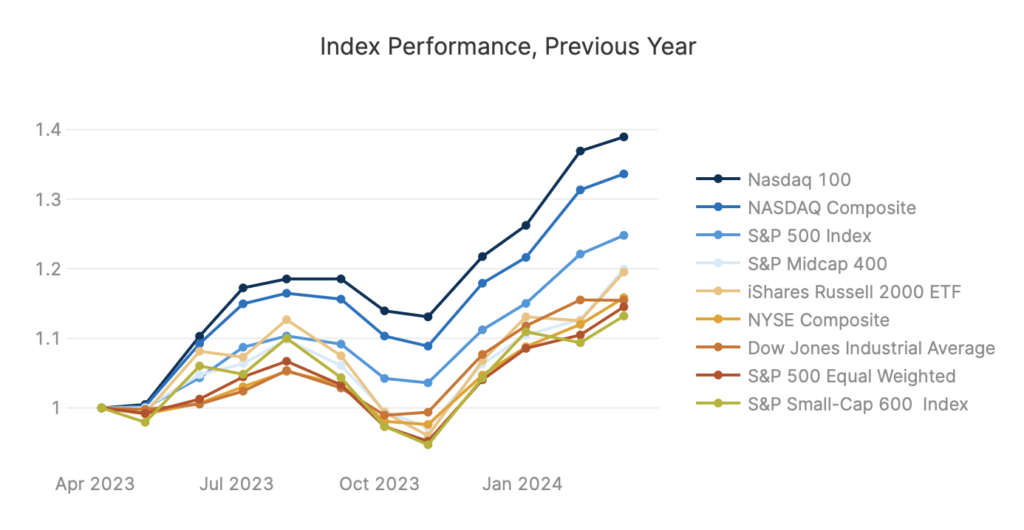

In Q1, technology took a step back as communication services (i.e. media and advertising) and industrials took the lead.

The technology and communication services indices are heavily skewed by the 7 megacap companies. AAPL and MSFT represent over 40% of technology, and META and GOOG are over 40% of communications services.

Notably the Nasdaq 100 and S&P 500 were not the top performers this quarter. The gains in the Nasdaq Composite and S&P Midcap 400 represent expanding market breadth.

The NASDAQ 100 is the big winner over the past year as enthusiasm about AI continues to benefit the megacap tech companies. These few companies represent an outsize share of US stock valuation and tend to skew indices with few stocks, such as the NASDAQ 100 or DOW 30.

Market Commentary: 2024 Q2

Chief Investment Officer

Table of Contents

Share

After taming inflation, the Fed aims for a soft landing

The market seems to have found a durable bottom in the fourth quarter of 2023. There was a strong rally at the beginning of November which included a wide variety of sectors and industries. Small and medium cap stocks benefited the most (as reflected by the indices), which contrasts significantly with their lagging performance over the previous year, as well as the narrow rally of last spring involving the tech giants. The businesses underlying small and medium stocks tend to be more sensitive to interest rates. We focus on these kinds of stocks and believe they provide great opportunities and value.

The long-expected recession still hasn’t arrived. The potential for weakness has caught the Federal Reserve’’s attention, however. In their December statement, the Fed indicated that they are anticipating 3 interest rate cuts toward the end of 2024. While the economy may remain healthy today, it’s worth remembering that rate cuts occur in response to an economic slowdown. A “soft landing” is the term given to a situation where the Fed manages to avoid a recession by acting right on time. These are rare, and the previous one occurred in 1995. (See chart below). The Fed is commonly perceived to react too late both to inflation and recession.

Looking ahead, we’re optimistic about the market. Just because the Fed sees the possibility for a slowdown, doesn’t mean it would occur soon. Additionally, there are some potential supports for the economy, which might help achieve a soft landing. These include pent-up housing demand and a wave of productivity gains from new technologies. There are of course risks to this scenario (including geopolitical risks), and we will continue to monitor new developments.

Active Manager Sentiment

April 4, 2024: 84.24% Aggregate Equity Exposure

After topping out at over 100% equity exposure, active managers trimmed positions to around 85% (in aggregate). We read this as a signal that the market was overbought in the short-term, but not necessarily a sign of longer-term weakness.

The NAAIM Exposure Index represents the average exposure to US Equity markets reported by members. NAAIM member firms are asked each Wednesday to provide a number which represents their overall equity exposure at the market close. Responses are tallied and averaged to provide the average long (or short) position of all NAAIM managers, as a group.

Disclosure: Magnifina is a frequent contributor to this index.

Stock Performance by Category

The NASDAQ 100 is the big winner over the past year as enthusiasm about AI continues to benefit the megacap tech companies. These few companies represent an outsize share of US stock valuation and tend to skew indices with few stocks, such as the NASDAQ 100 or DOW 30.

Get insights delivered to your inbox and never miss our latest research and key developments. Our monthly roundup includes analysis, updates, and other resources for serious investors.

Related Posts

Wendy’s stock and brand value arbitrate

Investing vs gambling and how to keep the casino out of your portfolio

Should you open a Trump account for your child’s education?

Are we right for you?

Take our brief survey to learn if our advisory services are the best match for your financial goals and situation, and see if we should move forward together.

Ready for the first step?

Schedule a no-cost consultation to discuss your financial goals and explore how we can help you build a personalized investment strategy.